Dividends decoded: your path to cash-flowing investments

Picture this: you own a slice of a successful company, and instead of just sitting on your ownership certificate hoping the price goes up someday, the company regularly deposits cash into your account as a "thank you" for being an investor. That's essentially what dividends are - your slice of the profit pie!

Dividends are like that friend who always pays you back - they represent tangible returns that companies share with their investors, typically every quarter (but it could be anything from monthly to yearly). So yes, it’s basically getting paid just for holding shares. Not bad, huh?

When a company's board of directors looks at the latest financial results and says, "Hey, we did pretty well! Let's share some of this success with our shareholders," that's when the dividend magic happens.

These payments can come as direct cash deposits or additional shares of stock (more ownership, more potential dividends - hello, snowball effect!).

Fun fact: the word "dividend" comes from the Latin term "dividendum", literally meaning "thing to be divided."

It is important to recognize that paying dividends is not considered an expense for a company but rather a division of after-tax profits among its owners.

Dividends: the sweet perks of holding on

Dividends are like the cherry on top for investors - those regular payouts can sweeten your portfolio with a steady stream of income without having to sell a single share. But dividends aren't a promise, they're a privilege. Companies dish them out when they’re feeling confident, cash-rich, and not in urgent need of reinvesting profits elsewhere.

Usually, dividend payments are a sign of maturity - think stable, established businesses that have already covered the basics (like reinvestment and R&D) and are now sharing the wealth. The more shares you own, the bigger your slice of the dividend pie. But timing matters. To snag a dividend, you’ve got to be officially listed as a shareholder by what's called the record date. This date varies by company and it's normally announced together with the intent (and amount) of paying dividends. On average you can expect it to be anywhere between 10 and 30 calendar days before the dividend payout.

Here’s where it gets interesting:

- A generous dividend can signal a company’s financial muscle and profitability.

- It also builds investor trust and boosts the company's reputation in the market.

- For income-focused investors - especially retirees - stocks with a strong dividend track record are pure gold.

And there’s more. Reinvesting those dividends means you're buying more shares with every payout, compounding your returns over time. It’s like planting a tree that keeps growing more fruit each season.

So while dividends may not grab headlines like IPOs or crypto swings, they play a quiet, powerful role in building long-term wealth. Think of them as your financial thank-you note from companies that value your trust.

Why companies pay dividends

Companies don't just pay dividends because they're feeling generous. There's strategy involved:

- Reward loyalty: paying regular dividends keeps investors happy and loyal.

- Signal financial strength: consistent dividends shout, "Hey we're financially stable!". This is especially true when a company that has troubles with revenue might tap into their profits (or cash) to distribute dividends in order to calm down investors. At the same time some investors might interpret it as a lack of promising new projects for future growth, suggesting the company is returning cash because it lacks better investment options.

- Attract investors: a steady stream of dividends makes a company attractive, particularly for investors craving consistent income. This increased investor interest can lead to higher demand for the company's stock, potentially driving its price upward.

- Use it or share it: when mature companies generate more cash than they have good investment opportunities for, they might think, "Well, rather than making a questionable acquisition or letting this cash sit around, let's give it back to our shareholders who might put it to better use".

Fun fact: February 2 is historically one of the most popular dates for companies to announce dividend increases, leading some financial analysts to call it "Dividend Groundhog Day".

Ultimately, a company's dividend policy can have a significant impact on its stock price and investor confidence. Once a company establishes a pattern of paying dividends, shareholders come to expect these payments, and any reduction or suspension can negatively impact investor confidence and potentially lead to a decrease in the stock's value. The dependability of dividends, especially during volatile market periods, provides investors with a sense of stability and can help to cushion against potential losses from price declines.

Yet, not every business pays dividends. Famous companies like Amazon, Biogen or Tesla don't pay dividends (at the time of writing), while others like Meta or Alphabet started paying dividends only recently.

Why companies don't pay dividends

Not all companies are dividend enthusiasts. Many - especially younger, faster-growing companies - prefer to channel their inner squirrels and reinvest everything back into the business:

- Tech titans and biotech companies often need massive capital to fuel research, development, and expansion. By reinvesting profits, these companies aim to increase their value and ultimately deliver returns to shareholders through capital appreciation of the stock price.

- Growth-focused companies believe (often correctly) that they can generate higher returns by reinvesting profits than shareholders could get elsewhere.

- Amazon and Berkshire Hathaway famously chose the "no dividend" path for decades, preferring to compound their earnings internally. This is based on the belief that they can deliver greater long-term value to shareholders through strategic reinvestments and acquisitions.

- Tax efficiency is another consideration - capital gains are generally only taxed when you sell, while dividends are typically taxed yearly.

However, a decision to not pay dividends can sometimes be influenced by other factors such as debt restrictions or financial difficulties, where conserving cash is paramount. As companies mature, they often transition from reinvesting everything to starting to pay dividends. It's like the company lifecycle: young companies need all their resources to grow, while established companies can afford to share.

Dividend yield: your investment's "interest rate"

Want to know how generous a company's dividend is compared to its stock price? That's where dividend yield comes in - it's basically the "interest rate" your stock investment pays you. The formula for dividend yield is straightforward:

Dividend Yield = (Annual Dividend Per Share ÷ Current Share Price) × 100

For example, if SuperCorp pays $2 in annual dividends and its shares cost $50, the yield is: ($2 ÷ $50) × 100 = 4%. This means for every $100 you invest, you'll receive about $4 per year in dividend payments. Not too bad!

In cases where a company pays dividends quarterly, the annual dividend per share is typically estimated by multiplying the latest quarterly dividend by four. For example consider a company that pays a quarterly dividend of $0.50 per share and has a current stock price of $40. The estimated annual dividend is $0.50 * 4 = $2.00. Therefore, the dividend yield would be ($2.00 / $40) * 100 = 5%.

The dividend yield is very useful because it gives you a sense of the income you will earn from dividends alone, without taking into account any potential capital gains from an increase in the stock's price.

But wait! A high yield isn't always great news. Sometimes it's a red flag. If a stock's price is plummeting (perhaps due to trouble at the company), the yield will automatically increase - even if the dividend amount stays the same.

Dividend investing: building your money machine

One strategy you could choose for your asset allocation then, is select companies that regularly pay dividends. If the amount is big enough, this could become an extra income or why not, even replace your entire salary and allow you to retire early - or simply allow you to change career without worrying about your salary.

Unlike growth investing, which centers on capital appreciation (target a stock price increase), dividend investing provides the dual advantage of income generation and the potential for long-term capital gains.

Dividend investing isn’t just about collecting regular income - it’s a clever, long-game strategy that blends stability, growth, and even a bit of tax magic. For starters, dividends can act as a stealthy hedge against inflation. When companies increase their payouts over time - and many solid dividend stocks do - it helps investors maintain the purchasing power of their income even as prices rise. In essence, your money isn’t just sitting pretty - it’s keeping pace with economic shifts.

Fun fact: Warren Buffett's Berkshire Hathaway receives over $5 billion annually in dividend payments from its investments, despite famously not paying dividends itself.

Now, let’s talk compounding. Reinvesting dividends - rather than spending them- is one of the most powerful wealth-building habits. Each payout buys you more shares, which in turn generate more dividends. Over time, this snowball effect can supercharge your total returns, often outpacing the performance of non-dividend strategies, especially during market lulls.

There’s also a bonus for the tax-savvy investor. In many countries, qualified dividends (it's a specific type) are taxed at lower rates than regular income. So while your money works for you, it may also be working smarter from a tax perspective.

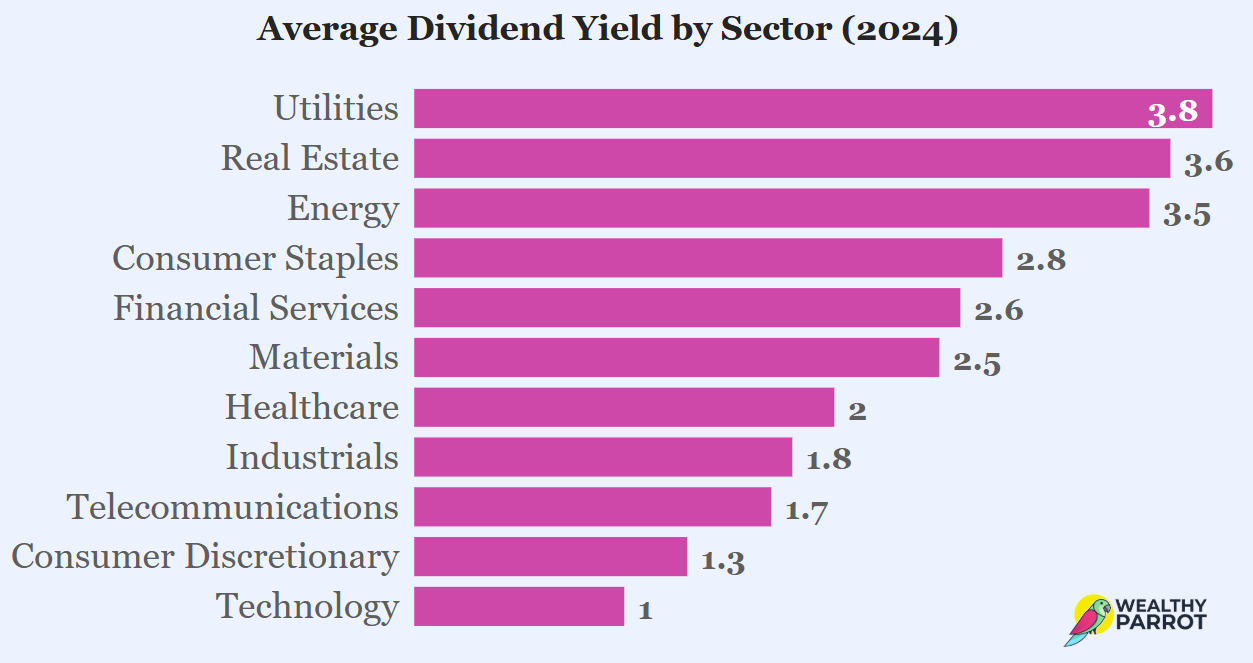

Lastly, dividend-paying stocks add a nice layer of diversification to your portfolio. While tech and growth stocks may steal the spotlight and be constantly on the news, dividend stalwarts are often found in sectors like utilities, consumer staples, and healthcare - industries known for stability and steady demand, no matter the economic weather.

Flavor options: different dividend strategies

Dividend investing isn’t a one-size-fits-all game - it’s a buffet of strategies, each with its own flavor and focus. One of the most popular approaches is dividend growth investing, where the spotlight is on companies that not only pay dividends but consistently raise them year after year. Over time, if you hold long enough, your yield on cost (dividends divided by the original price you paid) can grow dramatically, making it a compounding machine.

Another approach is high-yield dividend investing, where the goal is immediate cash flow. This strategy targets stocks with beefy dividend yields - perfect if you’re hunting for income now. But here’s the catch: when yields are too high, it could signal trouble. A crashing stock price or shaky business model might be inflating the yield, setting a trap for the unsuspecting investor. So, as always - due diligence is king. Look under the hood to make sure the payout is sustainable.

Then there's dividend value investing - a hybrid strategy that seeks out undervalued dividend payers. It's the best of both worlds: solid income and the potential for capital appreciation when the market catches up to a company's true worth.

Investing in Dividend Aristocrats is another popular strategy. Dividend Aristocrats are a select group of companies within the S&P 500 Index that have increased their annual dividend for at least 25 consecutive years. These companies are generally well-established, financially stable, and have a strong commitment to returning capital to shareholders, making them attractive for investors seeking reliable income and long-term stability.

Fun fact: if the aristocrats are not enough, "Dividend Kings" are S&P 500 companies that have increased their dividends for at least 50 consecutive years.

And let’s not forget dividend-focused ETFs and mutual funds, which package a basket of dividend payers into a single, diversified investment. Whether they focus on high yielders, dividend growers, or the Aristocrats themselves, these funds make it easy to follow a specific strategy without picking individual stocks. Some even come with built-in tax efficiency features, helping you keep more of what you earn - because hey, it’s not just what you make, it’s what you keep.

Before you dive In: the pre-dividend checklist

Before you jump into the dividend game, it’s smart to pause and look under the hood. Not all dividend-paying companies are created equal, and chasing a high yield without doing your homework can backfire. The key? Know your numbers and understand what they’re really telling you.

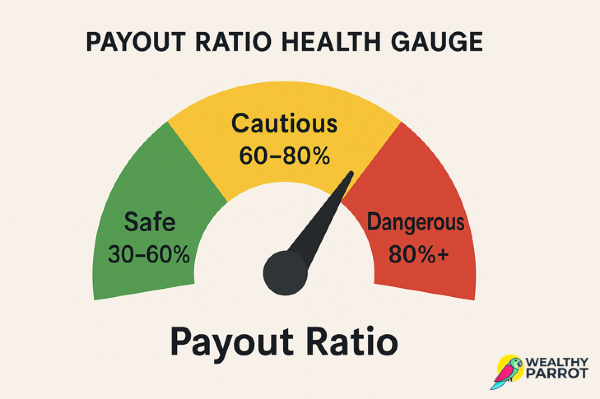

First up: financial health. One of the most telling metrics is the dividend payout ratio (DPR), which shows how much of a company's profit are being returned to shareholders.

A moderate ratio usually means the dividend is sustainable, with room left for reinvestment and future growth. But if the ratio is sky-high, that’s a red flag - it could mean the company is overcommitting and might struggle to maintain that payout down the road.

Closely related is the dividend coverage ratio (DCR), which measures how comfortably a company can pay dividends from its earnings.

Simply put, a higher dividend coverage ratio signals that a company earns significantly more than it’s paying out - giving investors extra confidence that dividends are safe, even during rough economic patches. Generally a value of 1.5 or higher is solid.

Fun fact: in 2008, during the financial crisis, some bank stocks briefly showed yields exceeding 20% before they inevitably cut their dividends, demonstrating why extremely high yields can be warning signs.

Then there’s free cash flow - the cash left after a company covers its capital expenditures. This is the real engine behind sustainable dividends. If a company consistently generates solid free cash flow, it’s more likely to maintain (or even boost) its dividends, even when earnings fluctuate.

Don’t forget the dividend history. Companies with long records of reliable or growing dividends - like the famous Dividend Aristocrats, who’ve raised payouts annually for at least 25 consecutive years - often have stable business models, strong cash flows, and shareholder-friendly management.

Another powerful tool in a dividend investor’s toolkit is the Dividend Reinvestment Plan (DRIP). The most common case is when your broker of choice allows you to reinvest dividends automatically (instead of pocketing cash dividends) - usually commission-free and sometimes at a discount. This helps supercharge compounding. But remember: those dividends are still taxable the year they’re paid, even if reinvested.

And speaking of taxes - don’t overlook them. Understanding qualified dividends (taxed at lower long-term capital gains rates) versus ordinary dividends (taxed as regular income) is crucial. Smart tax planning ensures you maximize the amount of cash you actually keep.

The dark side of dividend investing: what could go wrong?

Dividend investing can feel like a cozy financial security blanket - but even the best dividend strategy isn’t bulletproof. Before you start chasing yields, it’s important to be aware of some potential pitfalls that can put a dent in your portfolio or derail your income plans.

First, let’s talk market volatility. Even reliable dividend-paying stocks can experience significant price swings, especially during turbulent economic times. Just because a company pays dividends doesn’t mean its share price is immune to ups and downs. A sharp market drop can quickly erase your gains, even if dividends keep flowing.

Another big risk is the dreaded dividend cut or suspension. Companies distribute dividends from their profits - when times get tough, profits shrink, and dividends often become one of the first things on the chopping block. A sudden reduction or suspension of dividends can significantly hurt investors who rely heavily on that regular income.

Dividend investing can also inadvertently lead to sector concentration. Many dividend stocks cluster around industries like utilities, consumer staples, and real estate. If you’re not careful, you might end up too heavily invested in sectors that can underperform, reducing diversification and increasing risk. The same thing can happen with dividend reinvestment, that might lead to over-concentration in a single stock or cause you to buy more shares at inflated prices, especially during market peaks.

Fun fact: the oldest continuously paying dividend stock in the U.S. is York Water Company (YORW), which has paid dividends without interruption since 1816 – that's over 200 years of unbroken payments through wars, depressions, and pandemics.

Then there’s the opportunity cost factor. Dividend stocks tend to offer steady income, but they may not grow as rapidly as growth stocks that reinvest earnings back into their business. If you’re chasing rapid capital appreciation, dividend stocks might leave you feeling left behind.

Beware also of the dividend yield trap - a situation where a high dividend yield looks irresistible but is actually driven by a plummeting stock price or shaky finances. That seemingly juicy yield could signal trouble ahead, such as future dividend cuts or further share price declines.

Remember, dividends are never guaranteed. They’re at the mercy of management and the company’s board of directors, who can adjust dividend policy at any time based on business conditions or strategic priorities.

Lastly, watch out for inflation. Fixed or slow-growing dividends can lose purchasing power over time if increases don’t keep pace with rising costs. What seems generous today might feel disappointingly small down the road.

The takeaway? Dividend investing is powerful - but only if you go in with eyes wide open. Conduct thorough research, stay diversified, and always balance dividend stocks with your overall investment strategy.

The bottom line

Dividends aren’t just cash payments - they’re your slice of a company’s profits, making them one of the most appealing ways to invest. When companies decide to pay dividends, it’s a clear message about their financial health, strategic vision, and confidence in future growth.

Dividend investing offers some irresistible perks: steady cash flow, potential for long-term growth, and the magic of compounding through reinvestment. But, as with anything in investing, dividends come with their own set of risks and considerations. Smart investors know to look beyond yield and carefully examine a company’s financial strength, dividend history, and payout ratios to ensure sustainability.

Getting strategic about dividends means understanding different approaches - like dividend growth investing, where increasing payouts signal stable strength, or high-yield investing, which delivers immediate income but requires extra caution to avoid pitfalls. Don’t overlook tax considerations either; knowing how qualified dividends are treated versus ordinary dividends can significantly impact your after-tax returns.

At the end of the day, dividends can play a starring role in building your financial freedom - especially when combined with thoughtful research, balanced diversification, and smart risk management. With a well-crafted dividend strategy, you're not just investing - you’re actively growing your wealth, one payment at a time.

Happy investing! 🦜